Heart failure is an important global health concern both in high-income countries (HICs) and in low- and middle-income countries (LMICs) and affects approximately 64.3 million people worldwide. In HICs the prevalence of known heart failure is generally estimated at 1% to 2% of the general adult population. A Domus Medica publication gives additional information on the Belgian situation. The prevalence of HF increases as of 75 years of age. Between 70 and 80 years, the prevalence of HF ranges from 10 to 20%. In the total Belgian population, the yearly incidence of HF is 194 out of 100,000 inhabitants. For people over 50, this prevalence is 502 in 100,000 people, without a significant difference between men and women. In the USA, the estimated 2020 prevalence of HF is 6.9 million and is expected to increase to nearly 8.5 million in 2030 because of the growth of the US population.

In LMICs HF is associated with high morbidity and mortality, prolonged hospitalisation and consequently carries a high societal burden. The increasing incidence of HF in LMICs is driven by an epidemiological transition and a surge in the prevalence of aetiological factors such as hypertension, diabetes mellitus, dyslipidaemia or obesity and lifestyle changes characterised by decreased physical activity, increased alcohol intake and smoking.

2. Market Drivers & Trends / Opportunities

The global advanced therapy medicinal products ( ATMP) market size is expected to reach USD 21.2 billion by 2028. The market is expected to expand at a CAGR of 13.2% from 2021 to 2028. The ATMPs (Advanced Therapy Medicinal Products) exhibit the potential to cure diseases by addressing their root cause rather than symptomatic treatment. Thus, ATMPs help deliver transformative advantages which are not offered by conventional treatments. These factors are expected to drive the market over the forecast period.

The breakthrough FDA-approvals of Tecartus and Abecma post-approval of Zolgensma, Kymriah, and Yescarta have bolstered the exceptional advancements in this space. These approvals have spurred the investment flow in this arena thereby driving revenue growth. Key companies are adopting various operation models to accelerate the product manufacturing process.

Furthermore, the market witnessed several acquisitions by players that intended to enter or expand their existing business in this field. Acquisitions of Kite Pharma by Gilead Life Science, AveXis by Novartis, and Juno Therapeutics by Celgene are some major & recent examples. The most recent is the partnership between Novo Nordisk and Heartseed. These acquisitions depict the increasing interest of well-established pharma companies in this market.

Increasing competition for gene therapy buyouts can lead to hefty premiums.

On the other hand, with the growing consumer demands, the ATMP manufacturers are outsourcing their product manufacturing thereby creating lucrative opportunities for the contract manufacturing organisations. Thus, several CDMOs have expanded their facilities. For instance, in January 2021, FUJIFILM Diosynth Biotechnologies invested USD 40 million for the establishment of a new process development and manufacturing facility for advanced therapies and viral vectors.

· The cell therapy segment accounted for the largest revenue share in 2020 owing to the presence of a high number of approved products in this segment

· Increased investment flow to sponsor clinical trials has also spurred the revenue share of the cell therapy segment.

· Introduction of effective guidelines to support cell therapy manufacturing and the recent approval of advanced therapies further aid in the dominance of the segment

· The geographical expansion of Yescarta and Kymriah in Japan and Europe has encouraged the investors to support the development in this space

· Recent approvals of gene therapies have significantly accelerated the clinical trials in this segment.

· COVID-19 pandemic has opened new areas for key players to invest in T-cell research for viral infections.

· The research community is actively evaluating the potential of advanced therapies in COVID-19 patients, thereby aiding in market growth.

· North America accounted for the largest revenue share in 2020 owing to the exponential rise in clinical trials pertaining to advanced therapies.

· Strong pipeline of ATMPs in the U.S. accelerated revenue generation in the region

· Also, the shifting focus of U.S.-based companies from conventional drug development to ATMPs is driving regional growth.

· In Asia Pacific, the market is expected to witness the fastest CAGR owing to expanding ATMP landscape in emerging markets such as China at the forefront.

· Expanding business of China-based CDMOs has driven regional market growth

· Key companies are undertaking various strategic initiatives to maintain their market position. Collaboration between ViGeneron GmbH and Biogen Inc. in January 2021 is one of the notable examples of collaboration in this space.

· The companies collaborated on the development of an AAV-based gene therapy product for the treatment of inherited eye diseases.

3. Target market

Geographically, CASC8 will focus on high-income countries in Europe and USA, given the high price of the treatment. This patient group can be further segmented based on age (over 50 years), with a prevalence of 2%, and using left ventricular ejection fraction (LVEF) as phenotypic marker indicating underlying pathophysiological mechanisms and sensitivity to therapy.

Heart failure patients are often categorized as having HF with reduced (HFrEF; LVEF <40%), mid-range (HFmrEF; LVEF 40 – 49%), or preserved ejection fraction (HFpEF; LVEF ≥50%). Cut-off values are arbitrary and differ across guidelines. Most studies estimated that over half of all HF patients in the general population have a preserved LVEF and that this proportion is increasing. The clinical studies will provide insight in the subgroup who is benefiting the most of CASC technology.

The potential number of patients with HFrEF & HFmrEF is conservatively estimated at 2.5 million, based on:

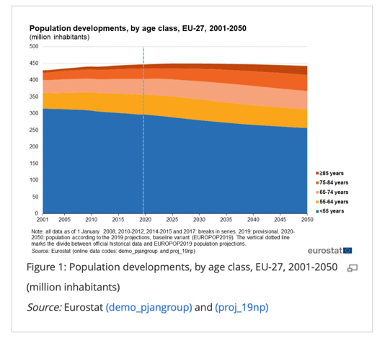

· Number of people older than 50:

o in EU-27: 150 million

o in USA: 117 million

· Prevalence of HF of 2%

· > 50% of all HF patients have preserved ejection fraction (40% of HF patients will potentially use CASC technology).

Population developments, by age class, EU-27 (million inhabitants)

If a penetration rate of CASC technology of 0.5% is considered, CASC therapy can be introduced in Europe to 12,500 patients. This can be gradually built up to 80,000 treatments/year (3%). The European market will be targeted first, but expansion to the USA will follow.

The price per treatment is assumed to be €145,000, leading to a potential yearly revenue of €11.6 billion (attainable market potential).

According to Seoane-Vazquez et al. (2019) the manufacturer price for an ATMP treatment ranges from US$ 18,950 for a tissue-engineered product to US$ 1,206,751 for a gene therapy. On average, prices are higher for gene therapy (US$ 357,309 – US$ 1,206,751) than for cell therapy (US$ 110,920 – US $814,780) and tissue-engineered products (US$ 18,950 – US $93,432). Yet, these prices do not include purchasing, inventory, and management costs that may significantly increase the overall treatment cost.

4.Pharmacoeconomics

The economic burden of HF on healthcare systems is considerable and will increase as the prevalence grows. An analysis in 2012 estimated the cost of HF to be $108 billion per year globally, with $65 billon (~60%) attributed to direct costs (medical costs) and $43 billon (~40%) to indirect costs (costs of lost productivity from morbidity and premature mortality). Also, the overall cost for HF increases as the stage of sickness increases which is influenced by the presence of diabetes mellitus, kidney dysfunction, COPD or hypertension.

In the USA, the total cost of care for HF in 2020 is estimated at $43.6 billion, with over 70% of costs attributed to medical costs. Urbich et al. stated that annual median total medical costs for HF care were estimated at $24,383 per patient in the US, with heart failure-specific hospitalizations driving costs (median $15,879 per patient). According to Lesyuk et al. (2018), for European countries like Spain and Poland these amounts are between $3,265 and $38,032, depending on the stage of HF (NYHA score), of which a large part is reserved for inpatient costs (43%).

5. Competitor Analysis

Current treatments for HF have been described in section 3.2. Several ATMP can be considered as competition for CASC technology, but none of them is available on the market yet.